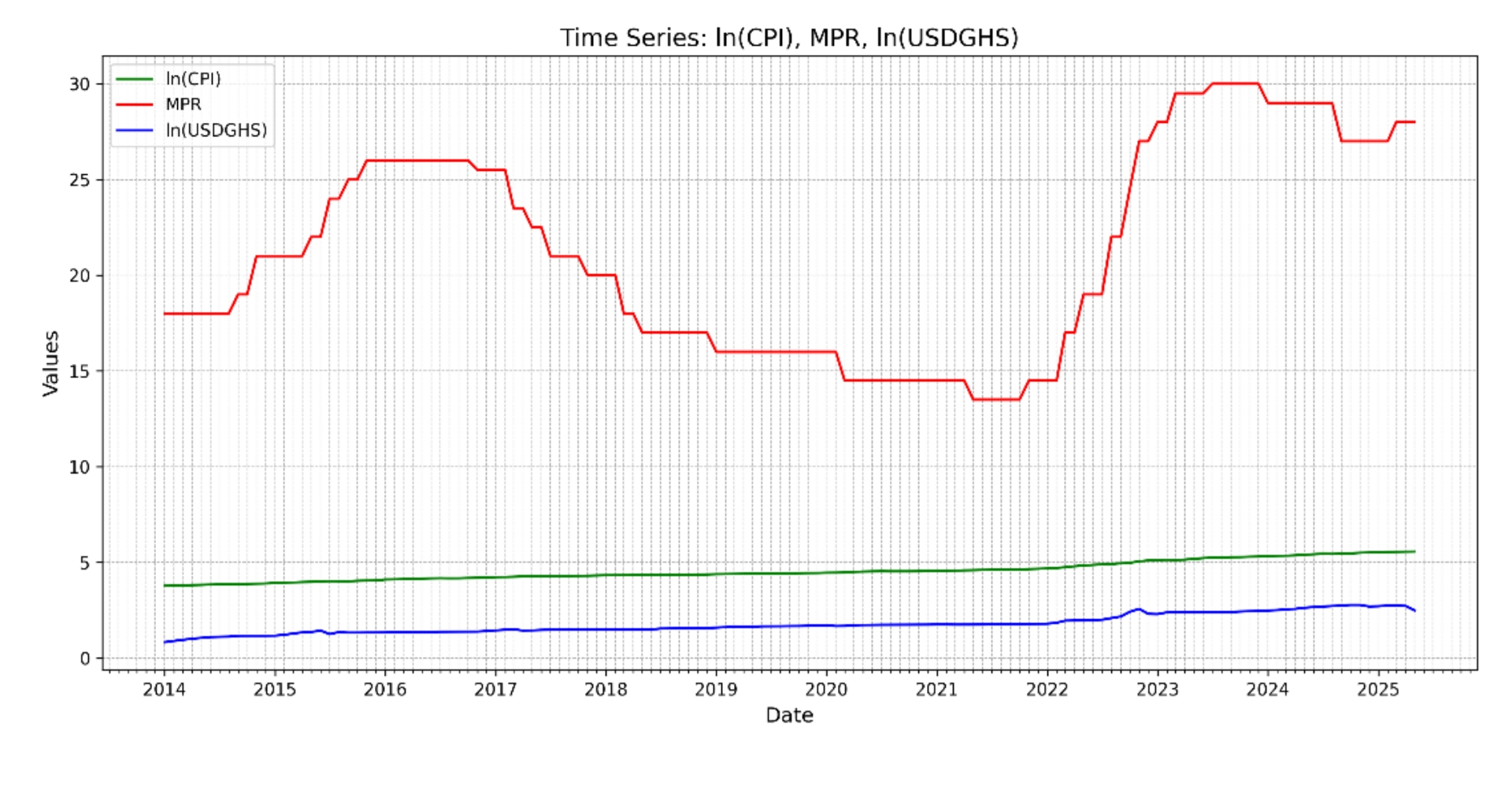

Modeling Inflation Jumps and Regimes in Ghana

Advanced Time Series Analysis | Macroeconomic Research

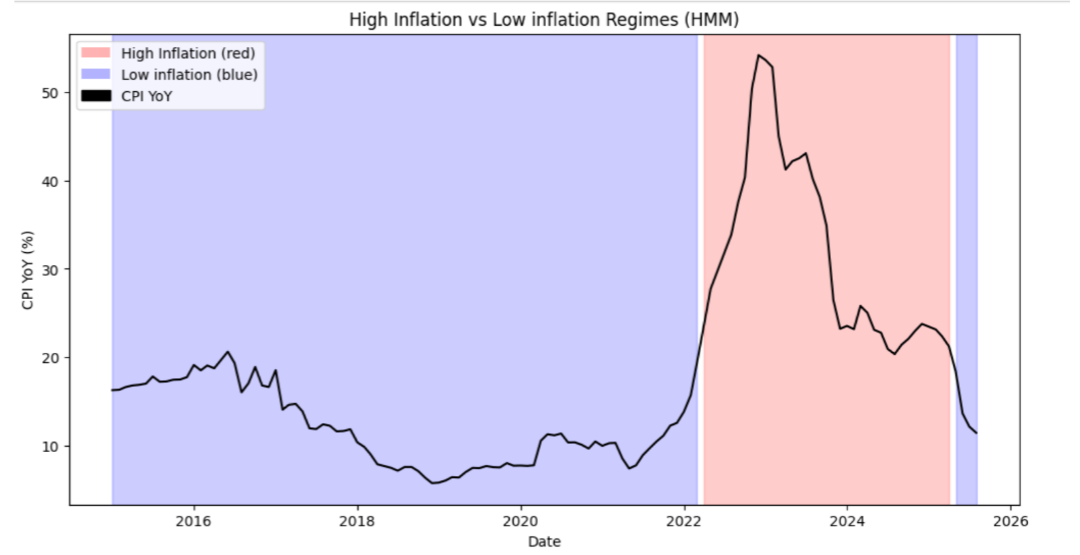

Methodology: Hidden Markov Models, Hawkes Processes, Change-point Detection

Examined regime shifts, structural jumps, and shock persistence in Ghana's inflation dynamics using sophisticated econometric techniques.

- Identified three distinct inflation regimes with precise timing

- Quantified endogenous vs. exogenous jump drivers (63.8% endogenous)